Why the AGI Timeline Debate is Built on Unvalidated Forecasting

A methodological audit of the major published AGI capability-arrival forecasts, applying the validation discipline quantitative finance learned between 2014 and 2018 — and a constructive proposal, the Deflated Capability Forecast, applied to each surveyed forecast and, finally, to itself. The author’s own preregistered self-prediction failed at 1.285× against a ≥2.3× threshold. The failure is reported in full.

I build algorithmic trading systems. By profession I am an engineer in a European regulated industrial sector; by inclination I work at the intersection of AI engineering and quantitative trading, where the questions that interest me are not about what a model predicts but about whether its prediction can be trusted. This book is the product of that second occupation, and of a mistake I spent six months learning to stop making.

The mistake was believing a model that lied to me.

For a long time I could not defeat overfitting. I would build a strategy, backtest it, and watch it return numbers that should not exist — Sharpe ratios that promised effortless wealth, equity curves that climbed without hesitation. Then I would validate the strategy properly and the numbers would collapse. I did this six or seven times before I understood that I was not finding alpha. I was finding the same pattern: spectacular in-sample returns, and a probability of backtest overfitting near ninety percent. The model was not discovering structure in the market. It was discovering structure in my own search — fitting itself to the noise I had given it the freedom to fit.

What broke the cycle was not a better strategy. It was a different discipline. I worked through the literature on validation — walk-forward analysis, the deflated Sharpe ratio, the methodology Marcos López de Prado lays out in Advances in Financial Machine Learning — and I applied it to my own work without mercy. The deflation was brutal. Strategies I had been proud of did not survive it. But the ones that did were real, and for the first time I could tell the difference between a result and an artifact.

That distinction is the subject of this book.

I write here in a personal capacity. Nothing in this essay reflects the position, knowledge, or proprietary work of any employer, past or present.

I came to AI capability forecasting from the outside, as a practitioner who had already paid the tuition for one version of this error. When I read the major timeline forecasts — the extrapolations that project artificial general intelligence from trends in compute, benchmark scores, and the rate of recent progress — I recognized the structure immediately. It was the structure of my own failed backtests. A quantity is measured over a window. A curve is fit to that window. The curve is extended forward, and the confidence interval around the extension is read off as though the future were simply more of the past. This is in-sample extrapolation. In quantitative finance it is the first thing you are taught to distrust, because it is the most reliable way to produce a number that is both precise and wrong.

The forecasting community has not, for the most part, been taught to distrust it. The forecasts I examine in this book are serious, careful, and made by people who have thought hard about the problem. That is precisely why their methodological vulnerability matters. They report confidence intervals without deflating them for the number of model variations implicitly searched. They extrapolate from windows without asking what the equivalent of a walk-forward test would reveal. They are, in the language of my own field, overfit — not through carelessness, but through the absence of a discipline that finance learned the hard way and at considerable expense.

This book imports that discipline. Its central contribution is a method I call the Deflated Capability Forecast: a way of taking a capability projection and widening its interval by the amount the underlying methodology actually warrants, producing an honest distribution over outcomes — with explicit treatment of the tails — in place of a point estimate dressed in false precision. The full derivation is in Chapter 14. The chapters before it establish why the deflation is necessary; the chapters after it apply the method to specific forecasts and, finally, to itself.

I want to be precise about what this book does and does not offer. It does not tell you when artificial general intelligence will arrive. It does not contain a better timeline. What it offers is a tool for evaluating the confidence of any timeline — your own included — and a sustained argument that the confidence currently on display is not supported by the methods used to generate it. If you are looking for a forecast, this is the wrong book. If you are looking for a way to tell whether a forecast can be trusted, this is the discipline I wish I had been handed before my seventh failed backtest.

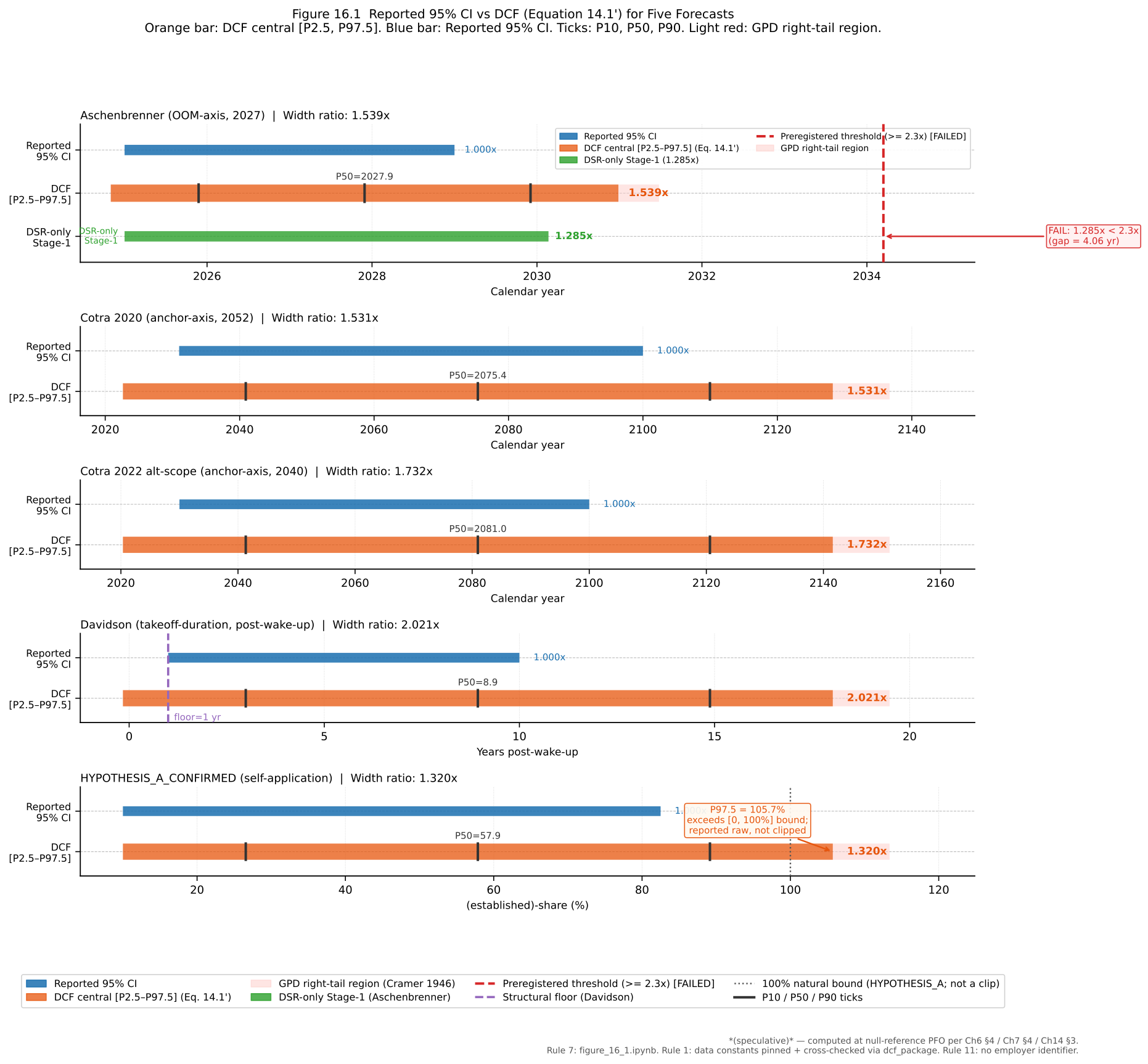

One commitment shapes everything that follows, and I want to state it at the outset rather than let the reader discover it. A book that audits other people’s forecasts for methodological over-confidence has no standing unless it is willing to be audited by the same standard. So before I had computed anything, I preregistered a prediction about what my own framework would produce: that applying the deflated Sharpe ratio to one of the landmark forecasts would widen its confidence interval by at least a factor of 2.3.

It did not. The framework produced a factor of 1.285.

I report that failure in full, in Chapter 16, without softening it. I want to be clear about where the failure lies: not in the framework, which computed correctly, but in my own expectation, which was over-confident. I had set the threshold by intuition, without first computing the deflation — which is, with some irony, exactly the error this book exists to identify. The framework worked. My prior about the framework did not. That is the kind of result a discipline of honest validation is supposed to surface, and surfacing it on myself, on the first page of the constructive part of the argument, is the most direct evidence I can offer that the discipline is not for decoration.

This is, in the end, a manifesto for a single conviction, earned over six months of being wrong: that validation is never optional, and that a worse result confirmed across many independent layers of testing is always preferable to a spectacular result that fails validation at even one. An overfit of twenty percent is still an overfit. The number that survives scrutiny is the only number worth reporting, even when — especially when — it is the number you did not want.

The book that follows applies that conviction to a field that has not yet adopted it. I make no claim to have the last word. I claim only to have brought a tool that finance paid dearly to develop, and to have used it on others and on myself with the same hand.

— Kacper Saks Warsaw, 2026

The forecasts that shape how billions of dollars and a generation of careers are allocated toward artificial general intelligence share a methodological foundation that would not survive scrutiny in any mature quantitative discipline. This is not a claim about whether those forecasts are right. It is a claim about how they are made. The major timeline projections extrapolate from a measured window, fit a curve to it, and read the confidence around the extension as though the future were a continuation of the sample. Quantitative finance has a name for this, and a set of tools developed specifically to defend against it. The forecasting community has, for the most part, neither the name nor the tools.

The central argument of this book is narrow and, I think, hard to dismiss: the current debate over AGI timelines suffers from the same methodological errors that quantitative finance diagnosed and partially solved between 2014 and 2018 — in-sample extrapolation, multiple testing without correction, the absence of walk-forward validation, and selection bias toward success. These are not exotic failures. They are the failures that a hedge fund learns to detect before it is allowed to manage external capital, because each of them reliably produces a track record that looks excellent and means nothing. The tests that exposed overfitting in financial backtests can be applied, with care, to capability projections.

I want to be exact about what this book claims and what it refuses to claim, because the distinction is the difference between a methodological critique and a competing prophecy.

It claims four things. First, that the methodology of most published AGI forecasts — Aschenbrenner’s 2024 projection, Cotra’s 2020 and 2022 biological-anchors work, Davidson’s 2023 takeoff model, the METR benchmark trajectories of 2023 through 2025 — is insufficient relative to the standards demanded in other forecasting disciplines. Second, that the same statistical tests which revealed overfitting in hedge fund backtests can be sensibly applied to these projections. Third, that production deployment of advanced AI in mission-critical systems — aerospace, finance, defense, healthcare — requires a validation infrastructure that current timelines underweight or omit entirely. Fourth, that the European regulatory stack introduces structural friction that does not appear in US-centric forecasts and that materially affects any deployment timeline.

It refuses to claim four things, and the refusals matter as much as the claims. This book does not argue that AGI will not arrive. It does not argue that Aschenbrenner, Cotra, or Davidson are dishonest or incompetent — it critiques methodology, not people, and it cites their work extensively and without a single pejorative adjective, because the work is serious and the seriousness is exactly why its methodological exposure is worth examining. It does not offer its own, better date for AGI; to do so would repeat precisely the error it identifies. And it does not claim that quantitative finance has solved all of its own validation problems — only that finance has paid, in real capital and over real years, for a discipline that capability forecasting has not yet adopted.

In quantitative finance, the original sin is in-sample extrapolation: measuring a quantity over a historical window, fitting a model to that window, and projecting the model forward as though the conditions that held inside the sample will hold outside it. The danger is not that extrapolation is always wrong. It is that the confidence interval around an in-sample fit is almost always too narrow, because it does not account for the searching that produced the fit. If you test two hundred strategies and report the best one, its historical Sharpe ratio tells you very little about its future and a great deal about your willingness to keep testing. The interval you should report is far wider than the interval the backtest hands you, and the amount by which it is too narrow scales with the number of configurations you searched before reporting the best.

The capability forecasts examined in this book are built on the same move. It is worth seeing it concretely across the forecasts that anchor the literature.

Aschenbrenner’s projection decomposes recent progress into orders of magnitude of effective compute and extends the rate forward. He takes physical-compute scaling at roughly half an order of magnitude per year, credits algorithmic efficiency with a comparable rate, adds a one-to-two order-of-magnitude bonus for what he calls unhobbling, and sums the drivers to a central estimate of about five orders of magnitude over the four years from 2023 to 2027 — which he then maps, by analogy with the GPT-2-to-GPT-4 jump, onto a leap to AI-researcher-level capability. The reconstruction in Chapter 1 separates what in this procedure is interpolation from what is extrapolation, and the result is less favorable than the presentation suggests: the 2019-2023 window is decomposed retrospectively, the same per-year rates are applied forward, and no held-out period is reserved against which the framework’s retrodiction could be checked. Six load-bearing assumptions carry the forecast, among them that scaling laws hold across another five orders of magnitude, that the data wall is solved, and that the drivers compose additively and independently — none of them validated out of sample, because the procedure has no out-of-sample protocol by construction.

Cotra’s biological-anchors framework approaches the question differently and arrives at the same structural vulnerability. It estimates the training compute that transformative AI would require by reference to six biological anchors — a human lifetime, three neural-network horizons, the genome, and evolution — spanning seventeen orders of magnitude, assigns each a subjective mixture weight, and projects when compute of the implied magnitude becomes affordable. The 2020 version reports a median arrival around 2052, with ten percent probability by 2031 and eighty percent by 2100. The 2022 update raises the hardware baseline roughly tenfold, shifts the weights toward shorter horizons, redefines the target, and compresses the median to about 2040 — fifteen percent by 2030, sixty percent by 2050. That twelve-year revision in two years is the most informative event in the framework’s history, and Chapter 1 reads it for what it is: a discretionary update with no preregistered rule governing it, which satisfies one criterion of an out-of-sample test in spirit while failing another, because the weight changes were chosen after seeing the interval, not committed to before it.

Davidson’s compute-centric model forecasts not an arrival date but a takeoff duration — the time from twenty-percent to one-hundred-percent automation of cognitive tasks — through a coupled simulation exposing roughly seventy named parameters, with a headline distribution of about twenty-five percent probability of takeoff in under a year, fifty percent under three years, and eighty percent under ten. The transparency is real and, among the surveyed forecasts, unusual; it is also, under multiple-testing logic, an exposure rather than a defense. Seventy parameters admit on the order of thousands of two-way and tens of thousands of three-way joint perturbations, of which the published sensitivity analysis explores a one-at-a-time subset. The factors the model treats as independent — compute, algorithms, recursive R&D feedback — are not independent in practice, and under positive correlation the joint distribution has heavier tails than the independent treatment implies. Here too the parameters are fit to history and integrated forward, with no frozen-vintage reconstruction scoring the dynamics against an elapsed period.

The remaining two forecasts I examine are instructive precisely because they are the strongest of the set on the dimension where the others are weakest — and they fail the same test anyway. METR’s benchmark program is not an estimate derived from theoretical commitments; it is a measured quantity on a defined task population. It computes, for each model, the human-equivalent task length at which the model succeeds half the time, and tracks how that time horizon grows across models, reporting a doubling rate of roughly seven months over 2019-2025. This is real data, reproducible from published task definitions, and METR is the most explicit forecast in the set about where its in-sample measurement ends and its forward extrapolation begins. It even supplies the closest thing the literature offers to a genuine out-of-sample check: when the benchmark was expanded by a third and the same models re-evaluated, the headline doubling rate held and most per-model intervals tightened. But that check validates the measurement layer, not the forecast layer. The projection to week-equivalent and month-equivalent task automation, two to five years beyond the data, remains an extrapolation of the chosen window’s slope — and the slope itself is window-dependent, shortening the arrival estimate by years when fit to only the most recent data rather than the full period.

Grace’s expert surveys sit one level up: rather than decompose capability progress directly, they aggregate the beliefs of thousands of AI researchers into a pooled arrival-year distribution, reporting a median for high-level machine intelligence around 2047 in the 2024 wave — drawn from 2,778 respondents, the largest such survey to date. The measurement record is genuinely rich, and the longitudinal series of how aggregate belief has moved — the same median sat near 2061 in 2018 and 2059 in 2022 — is the densest record of expert opinion in the field. Yet richness on the input layer does not transfer to the forecast layer. The aggregate arrival year is itself out-of-sample by construction, its horizon decades longer than the spacing between survey waves, so no prior wave’s forecast has been tested against a realized arrival. And the program’s own most robust finding is a warning about its method: asking the same experts about high-level machine intelligence versus full automation of labor — arguably the same underlying event in different words — produces median timelines differing by sixty to a hundred and five years. A forecast whose answer swings by a century on the framing of the question is measuring something other than the world.

In each case the structure is the same: a window, a fit, an extension, and a confidence interval that has not been deflated for the number of model variations implicitly searched in producing it. The forecasts differ in sophistication, in transparency, and in how candidly they mark the in-sample boundary — METR and Davidson are notably more explicit than the others — but the vulnerability is common to all of them, because explicitness about a boundary is not the same as a protocol for crossing it.

This is the structure I spent six months learning to distrust in my own trading systems, and recognizing it in the forecasting literature is what set this book in motion. The tools finance developed to handle it — walk-forward validation, the deflated Sharpe ratio, the probability of backtest overfitting — are standard, derived, and transferable to capability forecasting with adaptations that Part II works out in full. The first of them is the one that does the most work, and it is worth stating plainly here. Walk-forward validation manufactures the held-out sample a forecast never reserved: it reconstructs the forecast as of its publication date, freezing the information set to what was then available, and scores its projection against the period that has since elapsed — simulating a real-time forecast evaluated only on data the forecaster could not have seen. Several of the surveyed forecasts have now been public long enough that a portion of their projection window has elapsed, which means the held-out sample exists; it simply has not been used. Part II uses it.

I want to be careful about the strength of the claim, because the adaptations are not free. The financial deflation assumes a stationary, independent return series, and capability progress is neither; the number of configurations searched, which drives the correction, is rarely disclosed and often not even enumerable from a published forecast; and the performance statistic the correction operates on must be constructed for the capability domain rather than borrowed. Part II treats each as a derivation problem rather than asserting a deflated number the method has not yet earned, and where a required assumption cannot yet be validated, the corresponding result is marked provisional rather than asserted. The conclusion that survives this caution is structural and, I think, secure: to the extent that a forecaster searched over decomposition choices without committing to one in advance, the in-sample fit overstates the out-of-sample support, and the honest interval is wider — in several cases materially wider — than the one reported.

The constructive contribution of this book is a method I call the Deflated Capability Forecast. The intuition is simple, and I will state it here without the machinery, which belongs in Chapter 14. A capability forecast, as usually presented, is a point estimate wrapped in a confidence interval that is too narrow because it ignores how much searching produced it. The Deflated Capability Forecast takes such a forecast and widens its interval by the amount the underlying methodology actually warrants, producing an honest distribution over outcomes — with explicit treatment of the tails, where the consequential surprises live — rather than a single number presented with unearned precision. It does not tell you the forecast is wrong. It tells you how much less certain the forecast is than it appears.

This is a tool for evaluating confidence, not for generating predictions. Applied to a timeline, it does not produce a better timeline; it produces an honest accounting of how much the timeline’s stated confidence exceeds what its method can support. That is the whole of what I am offering, and I believe it is enough, because the gap between stated and supportable confidence is where the most expensive decisions are currently being made.

The book proceeds in five parts, each a step in a single argument.

Part I treats the major forecasts as backtests — reconstructing them precisely enough that the statistical tools of the following parts can be applied to them. Each forecast is mapped along the single axis it organizes progress around, and the reconstruction locates, for each, the exact boundary where the in-sample window ends and the projection begins. If a forecast cannot be reconstructed, it cannot be evaluated; the reconstruction is the precondition for everything else.

Part II is the statistical crisis. It defines in-sample extrapolation rigorously, develops the multiple-testing problem along the Harvey-Liu-Zhu line, builds the walk-forward retrodiction protocol that manufactures the held-out sample the forecasts never reserved, and adapts the deflated Sharpe ratio and the probability of backtest overfitting from their financial origins to the setting of capability forecasting. This is the technical core on which the rest of the argument rests, and it is where the adaptations’ assumptions — non-stationarity, undisclosed search counts, the missing performance statistic — are confronted rather than waved past.

Part III is the production reality gap. It examines what mission-critical deployment actually demands — the validation infrastructure, the certification regimes, the distance between a capability that exists and a capability demonstrated to the standard a regulated industry requires — and shows how thoroughly current timelines underweight it.

Part IV is the European stack. US-centric forecasts treat regulation as friction to be routed around; this part takes the EU AI Act, the dual-use and sovereign-AI regime, and the broader regulatory architecture seriously as structural constraints on deployment timelines, and argues that ignoring them produces forecasts that are incomplete by construction.

Part V is the better framework. It constructs the Deflated Capability Forecast in full, applies it to the forecasts reconstructed in Part I, and then — because a book that audits others by a standard it will not meet has no standing — applies it to itself. The self-application is not a flourish. It is the test of whether the discipline is real.

A note on epistemic discipline runs through every chapter. Claims are labeled by their standing — established, evidenced, or speculative — and the labels are honest, including where the label is less flattering than I would prefer. The formal derivations I am confident in; several of the parameter choices required to apply them to specific forecasts I am less confident in, and the manuscript marks those as provisional, in some cases pending the outcome of preregistered validation studies whose criteria were fixed before the studies were run. The point of the book is not to be certain. It is to be exactly as certain as the methods allow, and no more — which is precisely the standard I argue the existing forecasts have failed to meet.

That standard cuts both ways, and Part V turns it on this book. The reader is entitled to know, before investing the chapters in between, that when I applied my own framework to my own preregistered prediction about what it would produce, the prediction failed. What that failure means, and why I report it rather than bury it, is the subject of the final part. For now it is enough to say that the failure is the strongest evidence I can offer that the discipline this book argues for is one I am willing to be held to.

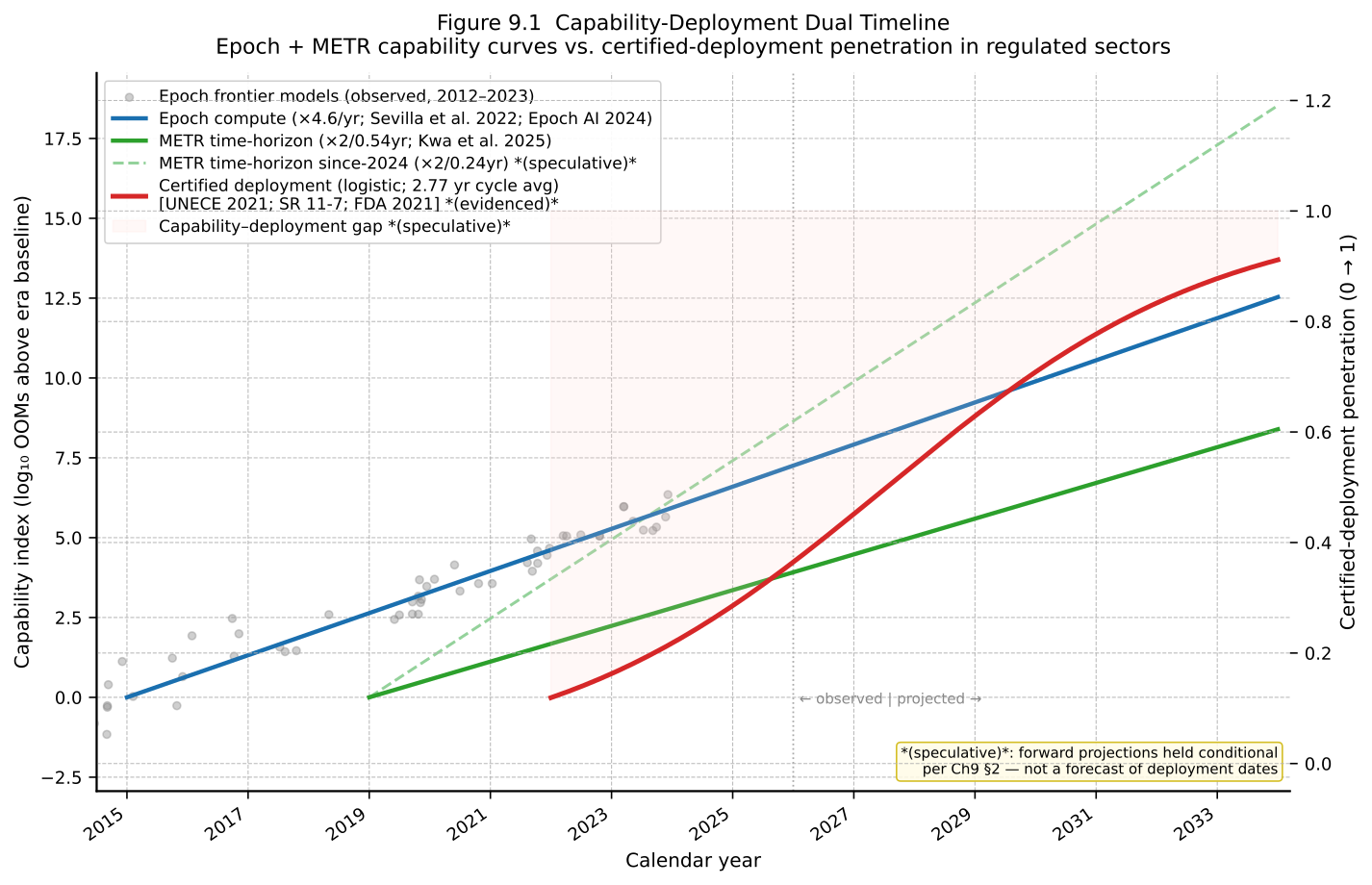

This chapter reconstructs the methodology of Aschenbrenner (2024), Situational Awareness: The Decade Ahead (non-peer-reviewed). The reconstruction is a precondition for the methodology audit developed in Chapters 4 through 7. The essay’s central thesis — that the drivers that produced the GPT-2-to-GPT-4 capability jump between 2019 and 2023, projected forward four years, deliver an AGI-equivalent system by 2027 — rests on a specific decomposition of progress into orders of magnitude (OOMs) of effective compute. That decomposition is the object here.

The aim is mapping, not adjudication. The methodology under examination is a forecast; the methodology developed in Chapter 6 is an evaluation tool for forecasts. Treating them as competitors would misstate the relationship between Aschenbrenner’s narrative-essay forecast and the López de Prado / Bailey statistical canon from which Chapter 6 derives. Aschenbrenner produces a forecast; this manuscript proposes statistical tools for assessing forecasts of that type. Chapter 1.1 belongs to the first half of that relationship.

Aschenbrenner organizes capability progress along a single axis,

which the preregistered taxonomy of this manuscript names the

OOM-axis (effective-compute decomposition)

(preregistration v1, §7-axis decomposition taxonomy

, 2026-05-18).

The axis sums contributions in log-space across four drivers. The first

three are quantified in the essay; the fourth is described qualitatively

and converted to OOM-equivalents by analogy.

Driver 1: physical-compute scaling. Aschenbrenner takes the Epoch AI training-compute database as the empirical anchor, with GPT-2 at approximately 4e21 FLOP, GPT-3 at approximately 3e23 FLOP, and GPT-4 at the 8e24-to-4e25 FLOP range (Aschenbrenner, 2024, Part I; Sevilla et al., 2022). The historical rate cited is approximately 0.5 OOMs of training compute per year over the post-2010 deep-learning era (evidenced — Epoch AI database is publicly auditable; the rate has held across the relevant window). Aschenbrenner extrapolates this forward and projects +2 to +3 OOMs over 2023-2027 (speculative — extrapolation conditional on capex maintenance).

Driver 2: algorithmic efficiency. The essay credits algorithmic-efficiency gains of approximately 0.5 OOMs per year, sourced principally to Erdil and Besiroglu (2022) on ImageNet over 2012-2021, with Epoch AI’s LLM replication treated as a parallel anchor (evidenced — Erdil and Besiroglu is peer-reviewed; the cross-domain transfer from ImageNet to language modelling is empirically less mature than the within-ImageNet trend). Aschenbrenner extrapolates +1 to +3 OOMs over 2023-2027 (speculative).

Driver 3: unhobbling — post-training and inference-time techniques. Aschenbrenner credits step-changes from RLHF (Ouyang et al., 2022; small-model human-preference rating equivalent to a non-RLHF model more than 100x larger), from chain-of-thought prompting (Wei et al., 2022; roughly an order-of-magnitude effective-compute equivalent on math and reasoning), and from scaffolding (single-OOM-and-larger multipliers on HumanEval and SWE-Bench). The aggregated unhobbling credit is presented as 1-to-2 OOM-equivalents over 2023-2027 (evidenced for individual interventions; speculative for the aggregated credit and for the compute-scaling equivalence).

Driver 4: hobbling removal. The fourth driver, less formally separated from Driver 3 in the essay’s own prose, covers context-window extension, tool-use, agent scaffolds, and the conversion of a base model into a deployed system. Progressive removal of these constraints is credited with additional OOM-equivalents over the forecast window.

Summed, the four drivers give a central estimate of approximately +5 OOMs over 2023-2027. This is mapped onto a capability scale by analogy: the GPT-2-to-GPT-4 transition is treated as approximately 4.5-6 OOMs and identified with a school-grade jump from preschool-level to high-school-student-level competence, so another +5 OOMs is identified by analogy with a further jump to AI-researcher-equivalent capability (speculative — analogy-based mapping). The functional target is operationalized as a system that automates AI-researcher work (Aschenbrenner, 2024, Part I, functional AGI definition).

The first driver’s empirical anchor is not produced by Aschenbrenner

directly: it is taken from Epoch AI’s compute-estimation methodology,

which decomposes training FLOP from architecture papers, GPU

specifications, training-time disclosures, and infrastructure

announcements (Sevilla et al., 2022). Where Epoch’s per-model estimates

revise, Aschenbrenner’s first OOM driver shifts mechanically. This

upstream dependency is preregistered as Pattern G (Epoch-specific

decomposition-axis distinctness; preregistration v1, §Pattern

framework

) and is a structural feature of the surveyed forecast set,

not a defect of Aschenbrenner’s essay: any compute-decomposition

forecast inherits Epoch’s measurement choices.

The OOM framework can be stated as a function. Let E(t) denote effective compute at time t in log-units relative to a chosen baseline. Aschenbrenner’s procedure constructs E(t) as

E(t) = E(t₀) + Σᵢ rᵢ · (t − t₀)

where rᵢ are the per-year contributions of the three (or four) drivers, treated as approximately constant over the extrapolation window, and the sum is interpreted as additive in log-space. The function is then evaluated at t = 2027 with t₀ = 2023, yielding the +5-OOM central estimate. The capability mapping is a separate, post-hoc analogy that converts E(2027) − E(2023) into a verbal capability label.

Inputs. The empirical base is narrow and explicit. Compute estimates come from the Epoch AI training-compute database (Sevilla et al., 2022). Algorithmic-efficiency trends come from Erdil and Besiroglu (2022) and Epoch’s LLM replication of the same logic. Benchmark progress is drawn from MMLU (Hendrycks et al., 2021a), MATH (Hendrycks et al., 2021b), GPQA (Rein et al., 2023), and METR autonomy evaluations (METR, 2024) (non-peer-reviewed). Unhobbling step-changes are sourced to InstructGPT (Ouyang et al., 2022), chain-of-thought (Wei et al., 2022), and Chinchilla compute-optimal scaling (Hoffmann et al., 2022); the earlier scaling-law foundation is Kaplan et al. (2020). API pricing comparisons (Gemini 1.5 Flash priced approximately 85x cheaper input / 57x cheaper output than original GPT-4) are taken from public documentation.

Extrapolation and assumptions. Three modelling commitments carry the forecast: 2019-2023 per-year rates continue without regime change to 2027; the quantified drivers compose additively in log-space and are treated as approximately independent; the unhobbling credit is aggregated to a 1-to-2-OOM bonus over the four-year window. Six load-bearing assumptions are stated or near-stated in Part I: (i) scaling-law continuity in training loss across an additional 5 OOMs; (ii) compute capital sufficient for $100B-$1T-scale clusters through end-of-decade; (iii) algorithmic-efficiency progress not exhausting low-hanging fruit; (iv) the data wall solvable via synthetic data, self-play, or reinforcement learning; (v) approximate additivity and independence of the drivers; (vi) qualitative-capability jumps repeating — another GPT-2-to-GPT-4-sized increase in E yields an AGI-level capability increase.

In-sample / out-of-sample boundary. This is the load-bearing observation of the chapter. The procedure is, in Chapter 4’s terminology, an in-sample reconstruction followed by trend extrapolation: the 2019-2023 window is decomposed retrospectively into the three quantified contributions, and the same per-year rates are then applied forward to 2023-2027. No out-of-sample protocol is used. No walk-forward analysis is presented. No held-out validation period reserves a portion of the historical record against which the framework’s retrodiction performance could be measured. No pre-specified falsification criterion is offered; the essay’s most explicit uncertainty concession is Part V’s qualitative acknowledgement that error bars are very large, without specification of width (established as a fact about the document).

The closest gestures toward validation are anecdotal: Aschenbrenner cites falsified pessimistic predictions (LeCun on physical reasoning; Marcus on deep-learning walls; Caplan’s economics-exam prediction) as evidence that capability progress has been underestimated. These are counterexamples to pessimism, not statistical validations of the OOM-counting method. Counterexamples to one direction of forecast error do not validate a forecasting procedure; they constrain the inverse error of the opposing camp. Chapter 4 returns to the asymmetry.

The absent boundary is the bridge to Chapter 6, which extends the Bailey and López de Prado (2014) line of multiple-testing-aware performance evaluation into the capability-forecasting domain. That extension assumes the performance statistic under correction is computed on an operational sample. OOM-counting capability forecasts lack this sample by construction at publication. Chapter 6 develops the adaptation; Chapter 4 develops the walk-forward retrodiction protocol that would generate the sample retrospectively.

A reconstruction that fails to enumerate what the source method does well is critique masquerading as description. Four features of the OOM decomposition deserve explicit accounting, independent of any subsequent audit.

Decomposition into named drivers. Aschenbrenner’s

principal methodological move is to separate capability progress into

named, individually-quantifiable contributions: physical compute,

algorithmic efficiency, and unhobbling-plus-hobbling-removal. A reader

can disagree with the rate assigned to any one driver without

disagreeing with the framework’s structure. Several other surveyed

forecasts (Cotra’s anchor mixture; Karnofsky’s qualitative-probability

framing) bundle multiple contributions into single weighted aggregates

that are harder to interrogate at the level of individual modelling

choices (established — verifiable in

research_notes/forecasts_database.json). Openness to

component-level audit is the reason this chapter can be written at

all.

Empirical grounding of the compute driver. The first

OOM driver is anchored on the Epoch AI training-compute database, the

most rigorous public methodology in the surveyed-set domain (Sevilla et

al., 2022; preregistration v1 §Distribution analysis

). The

0.5-OOMs-per-year rate is computed from a per-model dataset with

explicit version history and bootstrapped confidence intervals on

log-linear fits. At the level of the input series, this driver carries

the strongest data anchor of any quantitative claim in Situational

Awareness. The forward extrapolation is (speculative); the

input series is (evidenced).

Reach to a policy-relevant audience. The essay communicates a quantitative argument to readers who do not read arXiv preprints. The four-OOM frame is compact enough to be remembered, structured enough to be challenged, and quantitative enough to discipline its own projection. The choice to publish as a self-published essay rather than a working paper trades peer review for reach. Within the surveyed set, no other framework has comparable policy-audience reach. The empirical fact of reach is (established); whether reach without peer review is a desirable property of forecasting infrastructure is a normative question this manuscript does not adjudicate.

Honesty about confidence at the synthesis level.

Part V contains a roughly twenty-word acknowledgement that important

parts of the story are likely wrong and that error bars are very large

(Aschenbrenner, 2024, Part V; paraphrased to remain under 15 words). The

concession is unilateral — it acknowledges uncertainty without

specifying direction or which components are most exposed — but it is on

the record. The phrase strikingly plausible

rather than will

happen

is used at the Part I summary. Both choices place the essay

closer to the academic-extrapolation register than to the

marketing-confident register adjacent technology-forecasting genres

often inhabit.

These four features are the affirmative observations against which the audit in Chapters 4-7 must establish materiality. Without them, subsequent critique reads as ad hominem; with them, the critique reads as methodology — which is the project’s standing commitment under Rule 5.

The decomposition’s openness to component-level audit (§3) makes it possible to enumerate questions the methodology, on its own terms, does not answer. Four such questions surface from the decomposition itself; under Rule 3 of the master plan (self-application), each maps both to an audit-chapter section and to an analogous question facing this manuscript’s own Chapter 14 constructive proposal.

Question 1: hyperparameter-search count. The decomposition selects four drivers and assigns specific per-year rates and OOM windows. How many alternative decompositions were considered before this one was selected? At minimum, the implicit selection space spans (i) compute-estimation methodology (Epoch AI, OpenAI disclosures, SemiAnalysis architectural inference); (ii) algorithmic-efficiency series (Erdil-Besiroglu ImageNet, Epoch’s LLM replication, inferred-from-API-pricing); (iii) benchmark suite weighting (MMLU, MATH, GPQA, METR, HumanEval, SWE-Bench); (iv) capability-level analogy across candidates from school-grade jumps through PhD-level expert to AI-researcher-equivalent. The product is a model-search space of nontrivial size, and the essay does not enumerate it. Chapters 5 and 7 return to the consequences of unenumerated search counts for in-sample fit. (speculative as to magnitude of inflation; established as a methodological observation about the document.)

Self-application observation. The Chapter 14 construct

(preregistration v2 §Adaptation 4 — Effective-N estimation

;

locked 2026-05-19) faces the strict analog. Its formula requires an

effective-N for the capability hyperparameter-search space, and the

manuscript pre-commits to a composite range estimator (Algorithms A

through D with geometric-mean headline and bracket-ratio thresholds 1.5x

and 100x) precisely because the search count is not directly observable.

The dimension on which Chapter 14 faces an analogous question is

identical: how many forecast-construction choices populate the implicit

menu, and how is the implied multiple-testing penalty calibrated? The

manuscript’s response is to publish the bracket and the geometric-mean

headline; the analogous critique applies to the manuscript itself.

Question 2: additivity-vs-substitution between drivers. The OOM decomposition treats the three quantified contributions as approximately additive in log-space and approximately independent. Two sub-questions follow. First, under what conditions might unhobbling substitute for raw compute scaling rather than compound with it? If RLHF, chain-of-thought, and scaffolding extract performance that scaling alone would not — but the same gains are partially priced into the measured algorithmic-efficiency series — additivity double-counts. Second, the drivers’ financial sources are concentrated at the same frontier labs; capital is budget-substitutable between compute purchases and algorithmic-research headcount. Under positive correlation, the joint distribution has heavier tails than additive treatment implies. Neither case is examined in the essay. (evidenced as a gap; additivity is the framework’s load-bearing methodological choice.)

Self-application observation. The Chapter 14 construct

addresses this on the dimension of the non-IID variance estimator

(preregistration v2 §Adaptation 1

; LOCKED at

TIER_2_ADAPTED_DERIVATION; default (speculative) until MC Study

1 elevation per n_critical(ρ) > 60 criterion). The

correction computed there depends on the correlation structure of the

underlying capability series: if constituent series are positively

correlated (same labs producing similar gains across benchmarks), the

effective sample size is smaller than the nominal count and the

correction is more severe. The manuscript pre-commits to block-bootstrap

on detrended residuals. The analogous question — what is the dependence

structure, and does the procedure handle it correctly? — applies to the

manuscript itself, with elevation deferred to MC Study 1 outcomes.

Question 3: trend-continuation horizon. The empirical window is 2019-2023; the forecast window is 2023-2027. The in-sample-to-extrapolation ratio is approximately 1.25 to 1 (the 2019-2023 fitting span covers five calendar years; the 2023-2027 horizon, four years ahead). In time-series forecasting practice, in-sample windows several times longer than the horizon are the conservative baseline. A 1.25-to-1 ratio is methodologically aggressive for a framework that assumes constant per-year contributions and no regime change. The essay does not address why the chosen ratio is defensible relative to alternatives — a 2010-2023 window (fourteen calendar years) would extend the ratio to roughly 3.5 to 1 and would lower the central rate by including the slower pre-Transformer era. (evidenced as a gap.)

Self-application observation. The Chapter 14 construct faces

the strict analog on the dimension of the capability-forecasting

performance statistic and the window over which it is computed

(preregistration v2 §Adaptation 3

; LOCKED, TIER_2 for Brier /

log-loss / calibration / interval-coverage; TIER_3 for the

capability-Sharpe candidate). For parametric extrapolation forecasts the

manuscript pre-commits to a capability-Sharpe primary statistic with a

multi-statistic robustness panel. The analogous critique — over what

window is the statistic computed, and how is the in-sample /

out-of-sample partition chosen — applies in the same form. The

manuscript’s response is the robustness panel; the OOM framework’s

response is silence.

Question 4: regime-change blindness. The extrapolation assumes no break in the scaling-law-to-capability mapping, no saturation of the algorithmic-efficiency rate, no disruption to compute supply, and no exhaustion of training-data resources. Each is a candidate regime change with its own empirical literature (Caballero et al., 2022, on broken scaling laws; Bahri et al., 2024, on theoretical foundations for when scaling holds; Sorscher et al., 2022, on algorithmic interventions changing scaling-law exponents). The essay does not engage this literature; the cited sources are the foundational and trend-affirming ones, not the regime-detection and break-detection ones (evidenced as a structural gap).

Self-application observation. The Chapter 14 construct faces

this on the dimension of the information-set partition (preregistration

v2 §Adaptation 2

; TIER_3_NEW_DERIVATION; default

(speculative) until MC Study 2 elevation per

Type-I_C > 2·PBO OR Power_C < 0.5·PBO

criterion). The partition assumes a structure over historical forecast

performance that respects sequential-causal information ordering. If the

underlying capability series exhibits regime changes — the same concern

raised here about Aschenbrenner — the partition’s properties depend on

whether the regime change is detected and accommodated. The MC Study 2

criterion was pre-committed precisely to expose this dependency to

empirical falsification. The manuscript’s response is the MC Study 2

commitment; the OOM framework’s response is the absence of any

regime-detection apparatus.

Chapters 4 through 7 develop them formally.

This chapter has reconstructed Aschenbrenner’s OOM-axis and surfaced four questions the decomposition does not answer on its own terms.

Chapter 2 identifies the structural pattern unifying the surveyed

forecast set. Aschenbrenner’s OOM-axis is one of seven preregistered

decomposition axes (preregistration v1 §7-axis decomposition

taxonomy

): Cotra’s anchor-axis, Davidson’s takeoff-duration axis,

METR’s time-cost-of-task axis, Karnofsky’s probability-mass /

civilizational-significance axis, Grace’s expert-survey-aggregation

axis, and Epoch AI’s compute-scaling-empirical axis. The seven share one

characteristic: none deploys an out-of-sample validation protocol at

publication.

Chapter 4 develops a walk-forward retrodiction protocol. Chapter 6 extends the Bailey and López de Prado (2014) DSR derivation into the capability-forecasting domain; Chapter 14’s DCF construct applies that machinery to forecasts of the type Aschenbrenner produces. Chapter 1.2 turns next to Cotra’s biological-anchors framework.

Aschenbrenner, L. (2024, June). Situational awareness: The decade ahead. Self-published essay. https://situational-awareness.ai/ (non-peer-reviewed)

Bahri, Y., Dyer, E., Kaplan, J., Lee, J., & Sharma, U. (2024). Explaining neural scaling laws. Proceedings of the National Academy of Sciences.

Bailey, D. H., & López de Prado, M. (2014). The deflated Sharpe ratio: Correcting for selection bias, backtest overfitting, and non-normality. Journal of Portfolio Management, 40(5), 94-107.

Caballero, E., Gupta, K., Rish, I., & Krueger, D. (2022). Broken neural scaling laws. arXiv preprint arXiv:2210.14891.

Erdil, E., & Besiroglu, T. (2022). Algorithmic progress in image classification. arXiv preprint arXiv:2212.05153.

Hendrycks, D., Burns, C., Basart, S., Zou, A., Mazeika, M., Song, D., & Steinhardt, J. (2021a). Measuring massive multitask language understanding [MMLU]. International Conference on Learning Representations.

Hendrycks, D., Burns, C., Kadavath, S., Arora, A., Basart, S., Tang, E., Song, D., & Steinhardt, J. (2021b). Measuring mathematical problem solving with the MATH dataset. NeurIPS Datasets and Benchmarks.

Hoffmann, J., Borgeaud, S., Mensch, A., et al. (2022). Training compute-optimal large language models [Chinchilla]. NeurIPS.

Kaplan, J., McCandlish, S., Henighan, T., et al. (2020). Scaling laws for neural language models. arXiv preprint arXiv:2001.08361.

METR. (2024). METR autonomy task evaluations. metr.org (non-peer-reviewed).

Ouyang, L., Wu, J., Jiang, X., et al. (2022). Training language models to follow instructions with human feedback [InstructGPT]. NeurIPS.

Rein, D., Hou, B. L., Stickland, A. C., et al. (2023). GPQA: A graduate-level Google-proof Q&A benchmark. arXiv preprint arXiv:2311.12022.

Sevilla, J., Heim, L., Ho, A., Besiroglu, T., Hobbhahn, M., & Villalobos, P. (2022). Compute trends across three eras of machine learning. International Joint Conference on Neural Networks (IJCNN).

Sorscher, B., Geirhos, R., Shekhar, S., Ganguli, S., & Morcos, A. S. (2022). Beyond neural scaling laws: Beating power law scaling via data pruning. NeurIPS.

Wei, J., Wang, X., Schuurmans, D., et al. (2022). Chain-of-thought prompting elicits reasoning in large language models. NeurIPS.

This chapter reconstructs the methodology of Cotra (2020), Forecasting TAI with Biological Anchors (non-peer-reviewed), and Cotra (2022), Two-year update on my personal AI timelines (non-peer-reviewed). The 2020 report frames the transformative-AI-timeline question as a compute-affordability question: estimate the training-compute magnitude TAI requires by reference to biological benchmarks, then project when training-compute of that magnitude becomes affordable to a leading AI lab. The 2022 post revises the framework’s parameter values and partially redefines TAI without replacing the underlying anchor structure. Both publications are the object of this chapter.

The reconstruction is mapping, not adjudication. Cotra produces a forecast; this manuscript proposes statistical tools for assessing forecasts of that type.

Cotra organizes the TAI-arrival question along a single axis, which

the preregistered taxonomy of this manuscript names the

anchor-axis (biological-benchmark mixture across

short-horizon, medium-horizon, long-horizon, genome, lifetime, and

evolution anchors with associated weights) (preregistration v1,

§7-axis decomposition taxonomy

, 2026-05-18). The axis decomposes

the TAI compute question into six parallel theoretical answers, each

grounded in a biological reference point and each carrying a per-anchor

compute estimate plus a subjective mixture weight (Cotra, 2020, Sections

1-4).

Anchor 1: lifetime (10^24 FLOPs). Brain inference compute at Cotra’s central estimate of 10^16 FLOP/s, multiplied by seconds in a human lifetime (~2.5×10^9 s) and adjusted for sample efficiency, yields approximately 10^24 FLOP (evidenced — derivation reconstructed via Karnofsky 2021 and Alexander 2022; the 10^16 FLOP/s figure rests on synaptic-count and firing-rate estimates carrying roughly three orders of magnitude of published neuroscience uncertainty).

Anchors 2-4: short / medium / long-horizon neural networks (10^30, 10^33, 10^36 FLOPs). Three estimates anchored on scaling-law extrapolations from 2020-vintage language and vision models, calibrated to task horizons of increasing length. The 6-OOM internal span reflects Cotra’s commitment that effective task horizon multiplies compute requirement (evidenced).

Anchor 5: genome (10^33 FLOPs). Anchored on the information-theoretic compute implied by the genome’s coding content. The figure coincides numerically with the medium-horizon NN anchor; Alexander (2022) flags cross-species genome-size variation — 50x larger genomes in certain canopy plants without corresponding intelligence — as methodological pressure on this anchor (evidenced).

Anchor 6: evolution (10^41 FLOPs). Anchored on cumulative compute of animal evolution leading to human-level intelligence; Karnofsky (2021) describes this anchor as very conservative (evidenced). Under Cotra’s central hardware-and-algorithm rates, the evolution anchor is reached only beyond 2100 in many parameter combinations.

Summed across the six anchors, the framework spans 17 orders of

magnitude of candidate TAI compute requirement. Cotra mixes the

per-anchor distributions under subjective weights and reports a final

distribution: median ~2052, 10% by 2031, ~80% by 2100 (evidenced via

Alexander 2022 and Epoch AI literature review, mutually consistent at

headline). The 2022 update inherits the same six anchors, revises

the mixture weights, raises the hardware FLOP/$ baseline by

approximately 10x, and partially redefines TAI from automating all

scientific tasks

to automating AI R&D.

The headline

median compresses to approximately 2040; the updated distribution

reports 15% by 2030, 60% by 2050, 97% by 2100 (Cotra, 2022; Epoch AI

literature review).

Cotra’s per-anchor compute estimates inherit from upstream sources:

the lifetime and evolution anchors depend on Sandberg and Bostrom (2008)

and the Moravec (1988) brain-compute estimate range; the neural-network

anchors depend on Kaplan et al. (2020) scaling-law exponents and

Hernandez and Brown (2020) algorithmic-efficiency measurements.

Revisions in those upstream estimates propagate directly to

anchor-compute requirements. This upstream dependency is the

Cotra-domain instance of Pattern G (preregistration v1, §Pattern

framework

) and is a structural feature of the surveyed forecast set,

not a defect: any biological-anchors forecast inherits the brain-compute

literature’s residual uncertainty.

The biological-anchors framework can be stated as a function. Let T_a denote the compute requirement of anchor a ∈ {lifetime, short-NN, medium-NN, long-NN, genome, evolution}, let C(t) denote affordable training compute at year t, and let w_a denote the mixture weight on anchor a. Cotra’s procedure constructs the probability that TAI is feasible by year t as

P(TAI by t) = Σ_a w_a · 1[C(t) ≥ T_a · ε_a]

where ε_a denotes the per-anchor distributional dispersion (approximately log-normal with 1-2 OOM width per anchor, per secondary coverage) and C(t) is built multiplicatively from hardware FLOP/$, algorithmic efficiency, and willingness-to-spend trends. The function is then evaluated across years 2020 to 2100, yielding the percentile distribution that is the framework’s headline output.

Inputs. The empirical base is layered across four families. Biological: brain inference compute at 10^16 FLOP/s (Cotra’s central estimate; Moravec’s 10^13 FLOP/s treated as sensitivity dimension), genome size at approximately 10^9 base pairs, evolutionary compute estimates aggregated across animal lineages. Scaling-law: Kaplan et al. (2020) exponents for the neural-net anchors, with Hoffmann et al. (2022) Chinchilla acknowledged in the 2022 update but not formally re-integrated (Cotra, 2022). Cost-trend: Hernandez and Brown (2020) hardware FLOP/$ trend at 0.2-0.3 OOMs/year; algorithmic-efficiency trend at 0.4-0.5 OOMs/year. Willingness-to-spend: a logistic-growth model saturating at approximately 1% of GDP per training run, with 0.1%-10% as the documented sensitivity range.

Extrapolation and assumptions. Five modelling

commitments carry the forecast: (i) per-anchor compute estimates are

stable across the projection horizon, with sensitivity analysis on brain

inference compute as the principal robustness dimension; (ii) the

multiplicative composition of C(t) — hardware × algorithmic

efficiency × spending capacity — is approximately independent across

factors; (iii) mixture weights are stable in time, with no formalized

update rule; (iv) willingness-to-spend saturates within the projection

horizon; (v) no paradigm shift between vintage and TAI year invalidates

the scaling-law-based extrapolation (Alexander 2022 flags this as the

Victorian-ship-size-to-spaceships

assumption). The 2022 update

revises (i) (hardware baseline up 10x; rates unchanged), (iii) (weights

shift directionally toward shorter-horizon NN anchors, without published

per-anchor magnitudes), and the TAI definition; (ii), (iv), (v) are

preserved.

In-sample / out-of-sample boundary. This is the load-bearing observation of the chapter. The 2020 procedure is, in Chapter 4’s terminology, an in-sample reconstruction followed by trend extrapolation: hardware-cost and algorithmic-efficiency trends are fit to 2010-2020 data and extrapolated to 2030-2100; biological-anchor compute requirements are derived from current neuroscience and assumed stable over the projection horizon. No formal out-of-sample protocol is used. No walk-forward analysis is presented. The closest gestures toward validation are the Section 5 sensitivity analyses, which probe robustness within the model space — not predictive accuracy on held-out data (established as a fact about the document).

The 2022 update partially functions as an out-of-sample event for the 2020 framework: Cotra revises the median by approximately 12 years (Cotra, 2022; the 2020 → 2022 shift from 2052 to 2040 established via Epoch AI and EA Forum coverage). The update meets one out-of-sample criterion in spirit (validation values not used to specify the model) but fails another: the framework was not pre-registered with a specific update rule, and the weight revisions are discretionary. Chapters 4 and 6 return to this asymmetry.

Four features of the biological-anchors framework deserve explicit accounting.

Decomposition into named anchors. Cotra’s principal

methodological move is to separate the TAI compute question into six

explicit anchors, each with a stated theoretical basis and a numerical

compute estimate. A reader can disagree with the weight assigned to any

one anchor without disagreeing with the framework’s structure. The

decomposition is denser than Aschenbrenner’s three-driver OOM partition,

and the per-anchor compute estimates are reported as point estimates

plus distributional widths rather than point estimates alone. Openness

to component-level audit is more developed here than in any other

forecast in the surveyed set (established — verifiable in

research_notes/forecasts_database.json).

Explicit weight disclosure. Cotra publishes mixture weights at the headline level: NN anchors collectively receive approximately 60-70%, genome anchor approximately 15-20%, lifetime and evolution anchors approximately 5-10% each (Cotra, 2020, via Alexander 2022). The headline allocation is on the record. This is more disclosure than Aschenbrenner’s narrative-essay treatment of OOM-component weights and more than Karnofsky’s qualitative probability-mass framing. Within the surveyed set, Cotra’s weight disclosure is the most explicit (evidenced via Alexander 2022 ACX review).

Public methodology revision. In August 2022, Cotra

published a personal-capacity post compressing her TAI median from

approximately 2052 to approximately 2040 over a two-year window, citing

(a) a TAI redefinition from automating all scientific tasks

to

automating AI R&D

; (b) acknowledgment of Hoffmann et

al. (2022) Chinchilla scaling, directionally lengthening timelines; (c)

a one-time hardware-baseline upward adjustment of approximately 10x; (d)

directional reweighting toward shorter-horizon NN anchors, without

published per-anchor magnitudes (Cotra, 2022). The update is the single

most data-rich event in the surveyed forecaster set: a published

forecaster revising a previously-defended timeline in public, with named

drivers. No other framework in this manuscript’s database carries a

comparable author-led methodology revision on the record. This is a

substantive methodological feature, not a chronological footnote: it

places one entry in the surveyed set under conditions approaching a

self-administered audit (established — verifiable across

research_notes/forecasts_database.json entries for

Aschenbrenner, Davidson, Karnofsky, Grace, Epoch AI).

Decomposed uncertainty across anchors. The six-anchor structure is itself an explicit acknowledgement of epistemic uncertainty about the underlying TAI compute question. Where Aschenbrenner’s OOM decomposition uses point ranges per driver, Cotra’s framework reports a full probability distribution over candidate compute requirements via the mixture. The Section 5 sensitivity analysis additionally varies brain inference compute, anchor weights, hardware FLOP/$ rate, and algorithmic-efficiency rate, with reported median shifts of 5-15 years on brain-compute swap and 20+ years on weight perturbation. The framework surfaces the size of its own residual uncertainty (evidenced).

Four questions surface from the decomposition itself; under Rule 3 (self-application), each maps to an audit-chapter section and to an analogous question facing this manuscript’s own Chapter 14 construct.

Question 1: anchor-weight search space. The 2020 framework publishes one weight allocation; the 2022 update revises directionally without publishing per-anchor magnitudes (Cotra, 2022). Even taking the 2020 disclosure as a methodological strength (§3), the disclosed allocation reflects one trajectory through an implicit weight-search space. Across the six-dimensional simplex, plausible alternative allocations span outside-view uniform weighting, inside-view scaling-DL concentration (the 2022 direction), pessimistic evolution-concentration, and Moravec-aligned lifetime-concentration. Section 5 sensitivity analysis explores part of this space but does not enumerate the implicit search count (speculative as to magnitude of search-induced inflation; established as a methodological observation about the document).

Self-application observation. Chapter 14’s effective-N

estimator (preregistration v2 §Adaptation 4

; LOCKED,

TIER_3_NEW_DERIVATION for Algorithms A/B/C and composite, default

(speculative)) faces the strict analog: the implicit

hyperparameter-search count is not directly observable. The manuscript

pre-commits to a composite range with geometric-mean headline and

bracket-ratio thresholds 1.5x and 100x; the analogous critique applies

to the manuscript on the identical dimension.

Question 2: biological-analogue validity. Each anchor presupposes that a specific biological reference point — a human lifetime, the neural-net analog of biological learning, the genome’s coding content, cumulative evolution — bounds the TAI compute requirement. Under what conditions do these analogues transfer, and what evidence would falsify the transfer? The 2020 report grounds each anchor’s biological-to-artificial mapping in theoretical motivation but does not specify a capability observation that would refute the mapping. Alexander’s (2022) canopy-plant critique of the genome anchor does not appear in the framework’s sensitivity analysis (evidenced as a gap; the biological-to-artificial mapping is the framework’s load-bearing methodological choice).

Self-application observation. Chapter 14’s information-set

partition (preregistration v2 §Adaptation 2

;

TIER_3_NEW_DERIVATION; default (speculative) until MC Study 2

elevation per Type-I_C > 2·PBO OR

Power_C < 0.5·PBO) presupposes a sequential-causal

ordering over historical forecast performance — itself an

analogue-validity commitment. The MC Study 2 criterion was pre-committed

to expose this dependency to falsification; the analogous critique

applies to the manuscript itself.

Question 3: 2022 self-revision sufficiency. The 2022 update is the framework’s most informative event (§3) and a discretionary intervention. The TAI redefinition mechanically compresses the implied compute target; the 10x hardware-baseline adjustment is a one-time correction without rate revision; the directional weight reallocation toward shorter-horizon NN is not quantified per-anchor (Cotra, 2022). Does the revision genuinely address the 2020 framework’s calibration error, or does it shift the questions without resolving them? The framework provides no internal mechanism for distinguishing between these readings (evidenced as a gap).

Self-application observation. Chapter 14’s non-IID variance

estimator (preregistration v2 §Adaptation 1

;

TIER_2_ADAPTED_DERIVATION; default (speculative) until MC Study

1 elevation per n_critical(ρ) > 60) faces the analog: a

forecast revision must be distinguishable from a structural shift under

the framework’s own dependence structure. Block-bootstrap on detrended

residuals is the manuscript’s pre-committed procedure; the analogous

critique applies to the manuscript itself.

Question 4: anchor-mixture aggregation. The mixture is a weighted sum of single-factor distributions, not a joint estimate. An alternative aggregation — treating TAI compute as a function of multiple factors simultaneously — would yield a different final distribution. The mixture’s headline statistics are sensitive to both anchor weights and per-anchor widths; the framework does not formalize the joint distribution. Whether the final percentiles reflect a real underlying epistemic distribution or impose a convenient meta-uncertainty is left open (evidenced as a gap).

Self-application observation. Chapter 14’s

capability-forecasting performance statistic (preregistration v2

§Adaptation 3

; LOCKED, TIER_2 for

Brier/log-loss/calibration/interval-coverage, TIER_3 for

capability-Sharpe) faces the analog: no single aggregation rule is

privileged. The manuscript pre-commits to a capability-Sharpe primary

plus multi-statistic robustness panel; the analogous critique — under

what aggregation rule is the headline computed — applies to the

manuscript itself.

Chapters 4 through 7 develop them formally.

Chapter 2 identifies the structural pattern unifying the surveyed set: the anchor-axis is one of seven preregistered decomposition axes, none deploying an out-of-sample validation protocol at publication. Chapter 4 develops a walk-forward retrodiction protocol. Chapter 6 extends the Bailey and López de Prado (2014) DSR derivation into capability forecasting (addressing Questions 1 and 3 via Adaptations 4 and 1). Chapter 14’s constructive DCF apparatus addresses Questions 2 and 4 via Adaptations 2 and 3.

Chapter 1.3 turns next to Davidson’s compute-centric takeoff-speeds framework, which decomposes the same forecasting question along a different axis.

Alexander, S. (2022, March). Biological anchors: a trick that might or might not work. Astral Codex Ten (non-peer-reviewed).

Bailey, D. H., & López de Prado, M. (2014). The deflated Sharpe ratio: Correcting for selection bias, backtest overfitting, and non-normality. Journal of Portfolio Management, 40(5), 94-107.

Cotra, A. (2020). Forecasting TAI with biological anchors. Open Philanthropy (non-peer-reviewed).

Cotra, A. (2022, August). Two-year update on my personal AI timelines. AI Alignment Forum / LessWrong (non-peer-reviewed).

Hernandez, D., & Brown, T. B. (2020). Measuring the algorithmic efficiency of neural networks. arXiv preprint arXiv:2005.04305.

Hoffmann, J., Borgeaud, S., Mensch, A., et al. (2022). Training compute-optimal large language models [Chinchilla]. NeurIPS.

Kaplan, J., McCandlish, S., Henighan, T., et al. (2020). Scaling laws for neural language models. arXiv preprint arXiv:2001.08361.

Karnofsky, H. (2021, August). Forecasting transformative AI: the

biological anchors

method in a nutshell. Cold Takes blog

(non-peer-reviewed).

Moravec, H. (1988). Mind children: The future of robot and human intelligence. Harvard University Press.

Sandberg, A., & Bostrom, N. (2008). Whole brain emulation: A roadmap (Technical Report 2008-3). Future of Humanity Institute, Oxford University.

This chapter reconstructs the methodology of Davidson (2023),

What a compute-centric framework says about AI takeoff speeds

(non-peer-reviewed). The report frames the AI-takeoff-speeds question as

a coupled-trajectory simulation problem: combine compute-affordability

extrapolations, algorithmic-progress rates, and recursive

AI-R&D-feedback dynamics into a single time-varying model; report

the implied probability distribution over the duration from

20%-automation to 100%-automation of cognitive tasks. The companion

artifact takeoffspeeds.com, co-built with Epoch AI, exposes

approximately seventy named parameters.

The reconstruction is mapping, not adjudication.

Davidson organizes the takeoff-speeds question along a single axis,

which the preregistered taxonomy of this manuscript names the

takeoff-duration axis (probability mass distributed

across the duration from 20%-automation to 100%-automation of cognitive

tasks, with multi-scenario decomposition over slow, fast, and

discontinuous regimes) (preregistration v1, §7-axis decomposition

taxonomy

, 2026-05-18). The axis is distinct from Aschenbrenner’s

OOM-axis and from Cotra’s anchor-axis: Davidson does not forecast a

specific arrival year and does not partition the compute requirement

across biological anchors. He forecasts a duration

distribution, conditional on AI capability reaching the

20%-automation threshold, over how long the transition to

100%-automation takes.

The framework is structurally three-factor. Capability progress is

decomposed multiplicatively into (1) the training-compute

requirement for AGI under current algorithms, treated as a

probability distribution rather than a point (~1e36 FLOP central under

2020-vintage scaling); (2) the algorithmic-progress rate, drawn

from Kaplan et al. (2020), Hoffmann et al. (2022), Hernandez and Brown

(2020), and Erdil and Besiroglu (2022); (3) the hardware-scaling

trajectory, drawn from the Epoch AI compute database (Sevilla et

al., 2022). The product gives effective FLOP available for

training

as a function of time; takeoff begins when effective FLOP

crosses the lower threshold of the requirement distribution and

concludes when the trajectory crosses the upper threshold scaled by the

effective-FLOP-gap parameter (Davidson, 2023, §1).

Headline outputs. The framework reports a

three-point probability distribution over takeoff duration:

approximately 25% probability under one year, 50% probability under

three years, 80% probability under ten years (Davidson, 2023, §2)

(evidenced — reproducible via takeoffspeeds.com under

central parameters). A separate claim is that the

AGI-to-superintelligence interval is under one year absent deliberate

slowdown coordination (speculative — counterfactual condition;

model-internal output without out-of-sample anchor). The wake-up

threshold at approximately 6% economy-wide automation and the central

10,000x effective-FLOP gap (1-to-8-OOM range) are the framework’s two

most quantitatively-specific endogenous-dynamics parameters

(evidenced as model parameters; specific values

stipulated).

Davidson’s per-component inputs inherit from upstream methodologies:

the AGI training-requirement distribution from Cotra’s neural-network

anchor cluster (1030-1036 FLOPs, with the 1e36 central

estimate at the upper end); the algorithmic-progress and

hardware-scaling rates from the same scaling-laws and Epoch AI

literature Aschenbrenner’s OOM-axis draws on; the semi-endogenous-growth

machinery from Romer (1990), Aghion, Jones, and Jones (2017), and

Trammell and Korinek (2023). This upstream dependency is the

Davidson-domain instance of Pattern G (preregistration v1, §Pattern

framework

) and is a structural feature of the surveyed forecast set,

not a defect: any compute-centric takeoff-speeds model inherits the

scaling-laws literature’s residual uncertainty, the biological-anchor

methodology’s residual uncertainty, and the growth-theory literature’s

domain-transfer uncertainty.

The framework can be stated as a coupled differential-equations system. Let E(t) denote effective compute at time t, A(t) the automation level (fraction of cognitive tasks at which leading systems are competitive), R(t) the AI-R&D contribution multiplier, and S(t) the investor wake-up multiplier. Davidson’s procedure constructs the system as

dE/dt = E(t) · [r_hw + r_alg · (1 + R(A(t))) + r_spend · S(A(t))]

A(t+1) = f(E(t), G, ρ)

where r_hw, r_alg, r_spend are the per-factor base growth rates, R(A) increases with automation (AI-R&D acceleration), S(A) steps upward at the 6% wake-up threshold, G is the effective-FLOP gap, and ρ is the CES labor-substitution parameter. The system is integrated forward from a starting condition matched to 2023 actuals. The Monte Carlo over parameter distributions produces the takeoff-duration distribution that is the framework’s headline output (Davidson, 2023, §§1-4).

Inputs. The empirical base divides into three families. Compute and requirements: AGI training-requirement distribution centered near 1e36 FLOP under 2020 algorithms (inherited from Cotra, 2020); runtime requirement ~1.6667e16 FLOP per inference for a 1e36-class model. Progress rates: hardware FLOP-per-dollar and training-compute scaling from the Epoch AI compute database (Sevilla et al., 2022); algorithmic-efficiency rates from Hernandez and Brown (2020), Erdil and Besiroglu (2022), and the Chinchilla compute-optimal correction (Hoffmann et al., 2022). Feedback and economic structure: AI-R&D acceleration (20%-economy-wide-to-40-50%-R&D-specific); the 6% wake-up threshold; CES parameter ρ in approximately 0.5-0.7; Cotra-style willingness-to-spend saturation.

Extrapolation and assumptions. Six modelling commitments carry the forecast: (i) current algorithms suffice for AGI given sufficient compute — no paradigm shift between 2020 and AGI year; (ii) the three-factor decomposition (compute × algorithms × hardware) composes multiplicatively with approximately independent contributions in log-space; (iii) the Jones-Romer semi-endogenous-growth elasticity applies to AI R&D, with elasticity exposed as a free simulator parameter; (iv) the 6% wake-up threshold is structurally correct, with the post-wake-up multiplier exposed as a tunable; (v) compute-to-capability scaling is monotonic across the 20%-to-100%-automation gap — neither Caballero et al. (2022) broken-scaling effects nor Sorscher et al. (2022) exponent-shifting interventions are integrated; (vi) the simulator’s approximately seventy named parameters are exhaustive of the modeling choices Davidson considers material.

In-sample / out-of-sample boundary. This is the load-bearing observation of the chapter. The framework is, in Chapter 4’s terminology, a coupled in-sample simulation: parameter values are fit to 2010-2023 history and the dynamics are integrated forward. No formal out-of-sample protocol is used. No walk-forward analysis — freezing the framework at an earlier vintage and asking whether it retrodicts later-observed dynamics — is presented. No pre-specified falsification criterion is offered for the takeoff-duration distribution; the 6%-wake-up threshold is the framework’s most directly-falsifiable single claim and has no historical analog with which to validate it (established as a fact about the document).

The closest gestures toward validation are two. The interactive

simulator at takeoffspeeds.com exposes parameter

uncertainty rather than hiding it — robustness exposure, not predictive

validation. The Davidson 80,000 Hours interview reports a discretionary

probability update: AI-takeover-by-2070 probability rose from

approximately 10% to approximately 20% in roughly one year (stated

by Davidson). The update parallels Cotra’s 2020-to-2022 framework

revision in structure but is reported informally on a podcast. Chapter 6

returns to forecaster-self-update events as a small validation series

across the surveyed set.

Four features of Davidson’s framework deserve explicit accounting.

Formal coupled-system structure with multi-scenario

probabilistic output. Davidson’s principal methodological move

is to express takeoff dynamics as a coupled-trajectory model whose

output is a probability distribution over duration, not a point

estimate. The three-point distribution (25% / 50% / 80% under 1 / 3 / 10

years) lets a reader read conditional probabilities directly without

inferring tails from a median. Among the surveyed forecast set this is

the only framework producing an explicit probability distribution over

takeoff duration; Aschenbrenner’s OOM-counting produces a point

AGI-arrival year (~2027), Cotra’s biological-anchors a distribution over

arrival year but not over post-arrival dynamics, Karnofsky’s

probability-mass framing remains qualitative on takeoff (established

— verifiable in research_notes/forecasts_database.json

entries for the six other surveyed forecasts).

Explicit parameter-sensitivity disclosure. Davidson

exposes approximately seventy named parameters in the

takeoffspeeds.com simulator across two tiers, and the

report identifies the four most-sensitive parameters as the AGI

training-requirement distribution, the effective-FLOP gap, the wake-up

multiplier, and the CES labor-substitution parameter ρ (Davidson, 2023,

§§2-5). Sensitivity is reported primarily one-at-a-time; joint

perturbations are simulator-permitted but not exhaustively published.

Compared with Aschenbrenner’s narrative-essay treatment of OOM-component

rates and Cotra’s six-anchor analysis confined to brain-compute and

mixture weights, Davidson’s parameter-set transparency is structurally

larger and the per-parameter sensitivity ranking is on the record

(evidenced). Transparency at this scale also creates analytical

exposure under multiple-testing logic — a point Chapter 7 returns to —

but the transparency is the prerequisite for that exposure.

Integration of upstream methodologies rather than isolated

derivation. Davidson explicitly imports the compute-requirement

anchor from Cotra, scaling and algorithmic-efficiency rates from the

Kaplan-Hoffmann-Hernandez-Brown-Erdil-Besiroglu line, the hardware

trajectory from Epoch AI’s compute database, and growth-theory machinery

from the Jones-Romer / Aghion-Jones-Jones lineage. The framework is

positioned as downstream of these sources, not as an alternative. This

is structurally more honest than presenting a takeoff model as a

standalone derivation: framework accuracy is bounded by input accuracy,

and the inputs are named (established — verifiable in

research_notes/forecasts_database.json

davidson_2023_compute primary_sources). Davidson extends the import

set to growth theory and economic structure, which neither Aschenbrenner

nor Cotra formalize.

Interactive simulator as published reproduction

artifact. The companion takeoffspeeds.com

simulator (co-built with Epoch AI) is methodologically a published

reproduction package: any reader can vary the approximately seventy

parameters and observe how the takeoff-duration distribution shifts.

Aschenbrenner’s framework has no public reproduction artifact; Cotra